SOL hit its highest price since May 2022, possibly due to an uptick in DApp use and a few other key factors.

Solana’s native token, SOL (SOL), experienced an impressive 22% surge on Nov. 10, breaking past the $54 mark for the first time since May 2022. Notably, this surge occurred amid the continuous selling of SOL tokens by FTX’s bankruptcy estate. The Delaware Bankruptcy Court approved the sale of the failed exchange’s assets, which included 55.75 million SOL, in September 2023.

Investor enthusiasm for SOL’s price increase may be attributed to the fact that some of the tokens from the bankruptcy proceedings are either vested or locked. Furthermore, there’s a weekly sale limit of $100 million imposed as part of the FTX liquidation plan. In essence, the initial fear of asset liquidation has transformed into hope as investors realize the limited impact of the sales.

FTX has been selling between 250k-700k $SOL every day for the last 2 weeks while price has either been going up or sideways.

so far its been getting absorbed like a champ and at current rate their unlocked tokens should be depleted within a week.

once this seller is gone i can… pic.twitter.com/AtnTqz3uxG

— Bluntz (@Bluntz_Capital) November 9, 2023

As trader and independent analyst Bluntz aptly described the situation, SOL’s resilience during the FTX bankruptcy token dump is impressive. The post on X (formerly Twitter) adds a bullish case for SOL, stating:

“Once this seller is gone, I can only imagine how hard it’s gonna pump.”

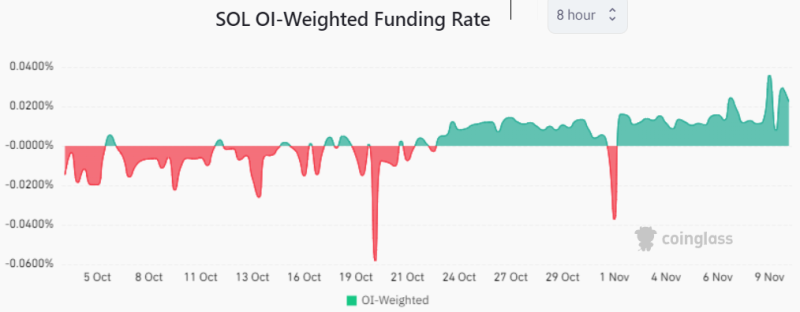

SOL price has been fueled by solid demand for leverage longs

SOL’s substantial 39% weekly gains have pushed its futures open interest to $745 million, the highest level since November 2021, when SOL achieved its all-time high of $260. Still, in futures markets, leverage longs and shorts are constantly matched, so it’s crucial to examine SOL’s funding rate for a more nuanced perspective.

A positive funding rate indicates that longs (buyers) demand more leverage, while the opposite occurs when shorts (sellers) require additional leverage, resulting in a negative funding rate.

SOL’s current futures funding rate represents a 0.5% weekly cost for leverage longs, which is not excessive given the prevailing bullish momentum. Yet, this is a significant shift from the funding rate levels observed three weeks earlier when leverage shorts were paying for leverage use.

While it could be argued that derivatives markets primarily drove SOL’s rally, there’s solid evidence indicating growth in terms of deposits and the usage of decentralized applications (DApps) within the Solana ecosystem.

Beyond derivatives, Solana’s ecosystem shows solid growth

Solana’s total value locked (TVL), which measures the amount deposited in its smart contracts, has reversed its declining trend after six consecutive weeks.

Solana’s DApps deposits have seen a 10% increase in the last three days. While the current 11.1 million SOL level is still below the 30 million SOL prior to the FTX exchange bankruptcy, this recent trend suggests that the worst period for the Solana network may be behind us.

it’sTo confirm that this movement isn’t solely driven by a few large holders inflating TVL, it’s essential to analyze the number of users employing active addresses as a proxy.

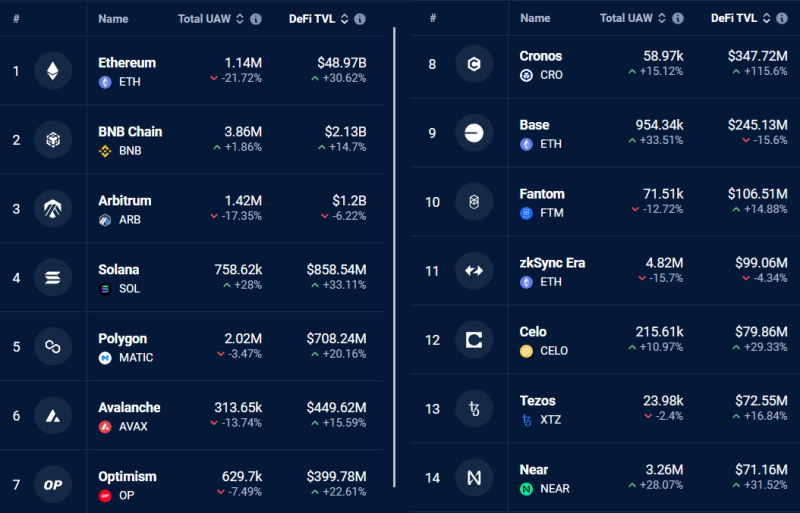

Solana now ranks as the fourth-largest blockchain in decentralized finance (DeFi) TVL, accompanied by a 28% growth in the number of active addresses. Interestingly, this surge in activity occurred while competitors experienced declines, with market leader Ethereum facing a 22% drop in DeFi active users, according to DappRadar.

On the one hand, SOL token bulls benefit from the increased network activity and higher TVL. On the other hand, Solana’s current market capitalization of $22.8 billion has surpassed Polygon’s $7.8 billion by nearly threefold, despite both networks having comparable DeFi TVL. This has prompted investors to question the sustainability of SOL’s bull run above $54.

Additionally, Solana protocol’s accumulated 30-day fees amounted to $1.9 million, compared to Polygon’s $1.6 million, according to DefiLlama. However, these figures pale compared to BNB Chain’s $9.1 million, raising doubts about the valuation after SOL’s recent rally.

As of now, there is no evident reason to bet against the trend, as there is no excessive leverage demand observed in SOL derivatives contracts. Nevertheless, the fundamentals hint at limited room for further upside.

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.