The past few months have seen a significant decline in Bitcoin’s volatility to multiyear lows.

- BTC’s annualized volatility fell to levels last seen in December 2016.

- However, Glassnode reported that this was not a new phenomenon.

Infamous for the significant volatility in its price, the past few months have been marked by volatility compression for the leading coin Bitcoin [BTC], Glassnode found in a new report. With most BTC trading sessions marked by “quietness,” “fewer than 5% of trading days have a tighter trade range,” the on-chain analytics firm noted.

Is your portfolio green? Check out the Bitcoin Profit Calculator

Mum says the market

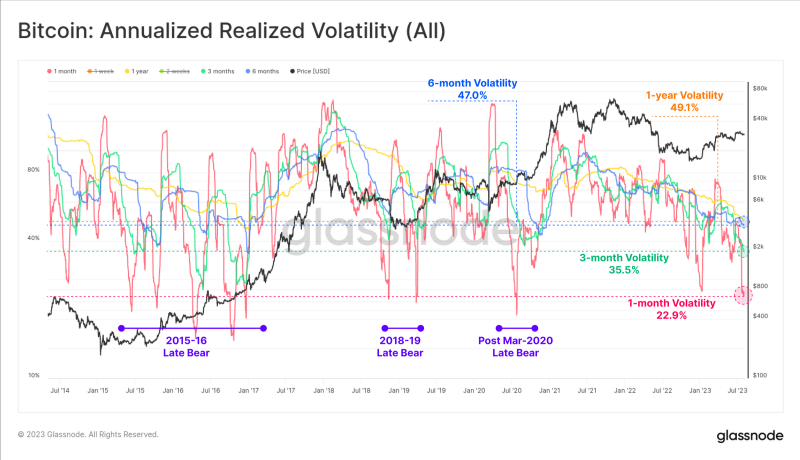

According to Glassnode, BTC’s annualized volatility has steadily declined this year. Observed within the 1-month to 1-year window period, this has fallen to levels last seen since December 2016.

Noting that this is not a new phenomenon, Glassnode highlighted four periods of extreme volatility compression in BTC’s price since 2015.

These included the late-stage 2015 bear market into the 2016 re-accumulation period, the late-stage 2018 bear market, which came before a 50% decline in November of the same year, March 2020 as the world grappled with the COVID-19 outbreak, and at the end of 2022 following the collapse of FTX.

Glassnode assessed BTC’s 7-day price high and low and found that these are only 3.6% apart. This refers to the highest and lowest prices the king coin has traded at over the past seven days. It is often used to gauge the coin’s price volatility and identify potential support and resistance levels.

At 3.6%, only 4.8% of its trading days have had a tighter weekly trade range since the coin began trading in 2009.

On a 30-day assessment, Glassnode found further:

“The 30-day price range is even more extreme, constricting price to just a 9.8% band over the last month, and with only 2.8% of all months being tighter. Periods of consolidation and price compression at this magnitude are extremely rare events for Bitcoin.”

Read Bitcoin’s [BTC] Price Prediction 2023-24

State of the derivatives market

Regarding volatility in BTC’s derivatives market, Glassnode found that volatility crush remains severe in the options market. Volatility crush describes the sharp decline in implied volatility, which is the market’s expectation of future price volatility.

Per Glassnode:

“Bitcoin markets are infamously volatile, with options trading at implied volatility between 60% to over 100% for the majority of 2021-22. However, at present, options are pricing in the smallest volatility premium in history, with IV (implied volatility) between 24% and 52%, less than half of the long-term baseline.